What is MLTA & MRTA?

Many first time home buyer is curious about the above while heading towards the property mortgage insurance.

Basically, both of them is referring to a mortgage assurance which is an insurance that cover repayment (loan) outstanding if you’re unable to do so such as death or total permanent disability.

Common 2 types: Mortgage Level Term Assurance (MLTA) and Mortgage Reducing Term Assurance (MRTA).

Having either one of the above will give you the peace of mind that in case anything happens to property owner, your dependents will not be burdened with settling your housing loan.

“Bank Negara Malaysia (BNM) doesn’t require mortgage insurance, many financial institutions are unlikely to approve mortgage to a home buyer if he/she doesn’t purchase an insurance policy”

The Difference

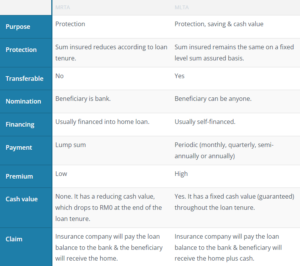

Mortgage Level Term Assurance (MLTA)

- Mortgage Level Term Assurance

- Protection against the property owner & able to transfer to other property.

- Offers repayment of outstanding loan as well as a guaranteed cash value.

- Higher policy premium

Mortgage Reducing Term Assurance (MRTA)

- Mortgage Reducing Term Assurance

- The most popular and economical option for property owner.

- Protection against the property address and owner only.

The Advantage & Disadvantage

Mortgage Level Term Assurance (MLTA)

- Require a higher premium in long run.

- Does not require upon purchase of the property, can buy it later.

- Age is the key role in MLTA much like life insurance, the higher the age, the higher your premium will be.

- Suitable for the sole breadwinner of your family and have several dependents.

- Suitable for property investor where the property is for the purpose of investment.

- Able transferable.

Mortgage Reducing Term Assurance (MRTA)

- Lower entry cost and commonly financial institution will factor the cost in the mortgage loan.

- Biggest downside is the loan settlement directly goes to the bank and does not provide any cash value for dependents.

- The coverage value fall below the home loan amount should take note that their MRTA will be affected by fluctuations in interest rates.

- Suitable for own stay where property owner plan to keep the house for the long term & also young adults who already have their own insurance.

Picture sources: imoney.my

The Tips

- Do not listen to the agents who try to throw in MRTA and/or MLTA in your housing loan package without justifying the needs.

- If you plan to sell the property within a few years, get MLTA instead of MRTA but if you intend to keep it for a long time the the other ways.

- Find out whether legal loan fees and valuation fees are financed in your mortgage loan package.

- If you plan to sell the property within a few years, do not purchase a mortgage insurance but if you intend to keep it for a long time or are co-purchasing it with someone else, then it is better to get the insurance.

- There is no need to purchase either insurance if you had a life insurance that covers the total amount of your loan and have no other financial pressure liability.

Disclaimer notice

The above contents is for information purpose only. Any views or opinions represented in this blog are personal and belong solely to HomeBrickz.com and do not represent those of people, institutions or organizations that the owner may or may not be associated with in professional or personal capacity, unless explicitly stated. The owner will not be liable for any errors or omissions in this information nor for the availability of this information.

No comment